VNV Global

A Swedish Venture Capital company. This company looks to have high upside potential. All things considered, it could be a 10X in 5 years!

Kicking off my Substack Series by writing a comprehensive review on VNV Global, brings me great joy! VNV Global is a SEK 3’000m market cap Swedish company, that currently holds successful brands like BlablaCar, Voi, and Gett just to name a few. This company looks to have high upside potential and it could be a 10X in 5 years. Granted there are some issues that could arise but, VNV Global is one to watch.

Below you will find 5 Questions (Asked and Answered) to provide you with a good overview of the company, covering the most important aspects. These Questions encapsulate a great summary of all the information I’ve been gathering on the company since 2019 (please note, information studied goes beyond that FY). Information was gathered from one on one calls with management, meetings with investors, tracking company communications (calls, CMD’s, etc), extracting reports, and analyzing public announcements, among others.

These are the 5 topics we’ll cover in this review:

1) The Company’s Business,

2) Moats and Advantages,

3) Alignment of Interest with Shareholders,

4) Valuation, and

5) Special considerations.

Let’s go!!

1) What does the company do?

The best way to describe VNV Global (formerly Vostok New Ventures) is to think of it as a Closed-End Venture Capital Fund that trades on the public market. The company’s NAV IRR from 2Q’12 until 4Q’22 is 17.6%, and the share price is currently around sek 26.00 (22nd of February 2023) trading at 53% discount to 4Q NAV/ share (sek 55.68).

As there is currently no need to give back liquidity to shareholders, unless they decide to do so (e.g. share buybacks and dividends), the company benefits from having permanent capital to invest and a long-term time horizon.

That said, in the financial report for 2022 the company announced that they would create a co-investment fund that will be focused on Series B deals. As explained by Per Brilioth, their CEO, it benefits the company (and hence, the shareholders) as it generates additional cash flow for the company but also provides more liquidity for VNV to invest in Series B companies. To investors of the fund (not the stock) it is also interesting as this move allows them to gain access to the deal flow while avoiding price fluctuations experienced in the stock market.

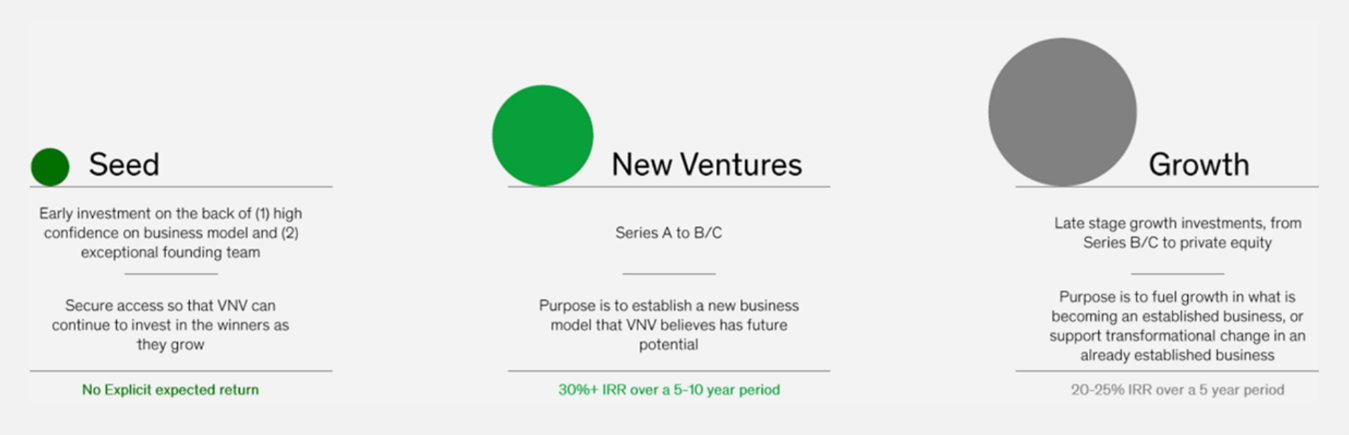

They are focused on the private market, investing in any company from seed until IPO, with a bottom-up approach and a 10+ year time horizon.

There are 3 key factors to determine whether to invest or not in each company VNV seek to have a holding in. 1) The investee is able to create high barriers to entry through strong network effects – which lead to natural monopolies. 2) It operates in a large market. And 3) the holding is led by strong founders – VNV sees themselves as investors in, not as managers of, their holdings; it’s their belief that the company’s management needs to be able to drive through the unexpected tailwinds inevitably encountered in business operations.

Below is a table taken from a VNV presentation regarding the governance, goals, and returns for each investment. It is important to mention that if a company is IPO’ed, and VNV is confident in the entity while expecting annualized IRR of 20%+ they may keep the holding; they benefit from the knowledge acquired over time (often years) from both the proximity with management as well as the business and unit economics of the company.

The portfolio is currently composed of 3 main sectors:

1) Classifieds/ Marketplaces (27%),

2) Mobility (54%) and

3) Digital Health (10%),

with “Others” being (9%). As they are agnostic to sector allocation, the current weights will certainly change.

2) Which competitive advantages and/or moats does the company have - if any?

The beginning of VNV’s reputation moat was the Avito investment back in the 2000s because they were early investors in the online classifieds space. Some very successful investments like Tinkoff and Hemnet kept adding fuel to the moat. I believe VNV’s approach to companies strengthens this moat even more as it is very supportive of the holdings, especially during downturns, with no desire to replace founders and their experience going along with companies through all stages (seed to IPO) – of which they can take full advantage.

Together with the reputation started early on, what I believe to be their most important moat is that VNV capitalizes from its own network effect, which I believe is widening while increasing in quality. They have been focused on looking for companies that show network effects for almost 2 decades now, and I would say they have been very successful, and they have built relationships within the industry and among other investors. These relationships have been increasing both in volume and quality, providing VNV with a steady flow of investing ideas. They also give them tools to support current holdings (e.g. connecting founders of business-related entities to each other).

On the other hand, currently, VNV companies have moats themselves (or can potentially create them), with the emphasis being on networking moats. This is especially important because we can find VNV to have individual moats (on the holdings), even if the company does not have any moats itself.

3) Are shareholders’ interests being safeguarded?

Per Brilioth, CEO and a key figure of VNV, has been in the company since 2001 and is the one who shaped the company as we know it today. Most of the moats (not to mention the investments made) came from his correct assessment of the opportunities presented to him.

Over the years we can see through annual and quarterly reports and calls that Per has been directionally correct regarding the holdings. Directionally doesn’t mean that things played out exactly as initially thought, but that as an aggregate he has been correct.

Outside of reports and calls, I also believe that people have a good opinion regarding Per and VNV’s management. This conclusion was derived from comments made by company founders in presentations and interviews, as well as opinions made by some other people I know personally who have had the chance to interact and work with Brilioth.

Even though I would prefer it if VNV Global were to have more liquidity currently, and to be net cash (more on that later), I believe the CEO has shown that he generally makes sound decisions managing VNV Global capital structure – i.e. spin-offs, share buybacks, dividends, and equity issuances.

Finally, I like it when CEOs have a stake in their company, valued more than 10x their annual wage (including bonuses). Currently, this is not the case for Per. There is a Long-term Incentive Plan in place but, I would love to see Per increase his stake in VNV with his own finances showcasing his confidence in the company’s future.

Concerning management, I would like to bring your attention to Björn von Silvers (joined September 2012) and Dennis Mohammad (joined last year). Besides their investment management capabilities, both have shown great availability and disposition to answer any questions, which I find to be very useful for a correct assessment of the company by (prospective) investors.

In a nutshell, I believe that management headed by Per Brilioth has indeed been creating value for shareholders.

4) How much may the company be worth? (Valuation)

The company delivered a 17.4% NAV IRR from 2Q 2012 until 4Q 2022, and this is despite the huge drop in NAV valuation of circa 59% from the peak (3Q’21) to the current bottom (4Q’22).

Will it drop more? Nobody knows.

However, if we assume the company does not go bankrupt and Per Brillioth keeps on being directionally correct (remember he has been in the company for 20+ years and has already lived through more than one global economic crisis, including the European Crisis and a few Russian crisis’s too…), with this kind of track record I think it’s safe to say we can make a few positive estimates.

A top overview:

Let’s first assume we hit the bottom of the NAV contraction. Assuming 17.4% CAGR is the new trend (below their hurdle rates for their investments), or a more “normal” growth trend of 22.5% (on their low end of the hurdles), we can all agree that the NAV could be (in the next 3 years) within a range of sek90 to sek102 and in 5 years within a range of sek124 to sek153.

Another way (more accurately) to value VNV global is by using a SOTP (Sum-Of-The-Parts) methodology. As most companies are private, the info available is pretty scarce. Still, Capital Markets Day of VNV over the years together with some info provided on calls and reports allow for some insights into some holdings shedding light on their value and makeup. Adding a 20% CAGR (again: minimum hurdle for VNV investments) for holdings that I couldn’t find data on, to accurately assign a value. I wouldn’t be surprised if NAV per share is sek 120 in 3 years and sek 300 in 5 years, or a 40% CAGR in 5 years. Likewise, I believe in a 5-7 year horizon the biggest holdings like BlablaCar, Voi, or Gett (on a standalone basis) could become more valuable than VNV’s current market cap.

It is interesting to note that the NAV calculated from SOTP would leave VNV’s NAV between the historical range of 20-30% IRR.

5) Any other special considerations to mention?

A deeper dive into the portfolio guides us to see that VNV is more diversified than it might appear at first glance. For instance, in the mobility sector, Blablacar – a car-sharing platform used mostly to move between cities, building a multimodal app, with a strong presence in Europe and Latam – is very distinct from Voi – scooters and bikes used to move within cities, whose presence is focused only in Europe. Similarly in marketplaces: where Booksy – a booking platform for services like Barber shops – is very different from Housing Anywhere – focused on renting homes; or in digital health, Babylon – a digital-first health service provider operating in the health business – differs from Numan – male health DTC app.

Regarding the balance sheet, I would also like to mention that currently, the company is in net debt (circa 15% of NAV). I am aware that having net debt can boost returns while at the same time permitting VNV to have more flexibility to invest now into the “winners of tomorrow” without the necessity of selling “current winners” for funding the future. Nevertheless, I like to be a bit more conservative, and I would prefer the company to rather be net cash and to have a stronger balance sheet.

Another thing to mention is the liquidity of the company. Currently, VNV’s liquidity is mainly being used for operating expenditures, coupons, and funding needs of holdings. A not-so-tight cash pile sitting on the balance sheet would certainly be much more appreciated, and excess cash could be used for share buy-backs given the current wide discount of market cap to NAV.

Unfortunately, this is not the case at the moment.

Nevertheless, there is good news.

Firstly, with moods changing in the investing environment, VNV’s companies are adapted and fastened to profitability. As said in VNV’s last call, 40% of the portfolio is currently profitable at an EBITDA level today, 40% will be profitable in the next 12 months, and only 20% will be profitable later than that. These changes will certainly increase the attractiveness of the company and its overall portfolio.

Secondly, as Per announced in the last 2 calls, there are several portfolio companies that may turn into liquidity this summer or by year-end 2023. I summed up some companies that may be of interest for others to buy and their aggregate weight comes close to 40% of NAV 4Q’22 – Gett which was just restructured, is EBITDA positive, and weights 20.6% in the portfolio could be one of them. I would also not discard some IPOs for 2023 or 2024 (e.g. BlablaCar). Lots of liquidity could be released and used for value creation (e.g. buy-back shares or on own/ prospective holdings at a much more attractive entry point than 1 or 2 years ago).

If this good news is delivered as expected, then some risk may be taken off the table. Therefore, it could work as a catalyst to share price appreciation, at least to NAV/ share which is where it is usually traded at.

In brief, I would prefer to see a higher management alignment of interests with shareholders, starting from Per Brilioth (the CEO) increasing his stake in the company. Also, I would much rather prefer the company be net cash (instead of net debt). As mentioned previously, even though leveraging the balance sheet can improve returns I prefer a conservative approach and for them to have a stronger foothold, ready for strong headwinds.

Concerning valuation, I hope the purpose of VNV's liquidity and debt function as expected. Nevertheless, in a worst-case scenario, I believe that buying shares at these low levels would still give positive returns even if a share issuance is to take place.

Price is currently around sek 26, this is a 53% discount to NAV/ share as of 4Q22. In theory, without further considerations, this means that if the company was to be broken down and sold in pieces one would double one’s investment made (circa +114%) after the debt was paid. It also means that if the company makes an equity issuance, even though it is highly dilutive to shareholders, I’d prefer that not to happen but, there is still some room until NAV/ share would become close to stock price, and from then on shareholders would be exposed only to fundamentals development.

Given current liquidity necessities as well as management’s track record, I believe there aren’t many reasons to think of, that would result in such a catastrophic situation.

In a base scenario. The sale (or an IPO) of a handful of companies over the next 6-12 months would both take some risk off the table while working as a catalyst for stock price appreciation. Giving some numbers to the range of outcomes, assuming no need for equity issuance and a NAV growth of 17.4% (the lowest assumption on VNV’s valuation explained earlier), price upside to NAV would be 247% (51% IRR) in 3 years and 378% (37% IRR) in 5 years. If instead, we use SOTP then we could get 362% (66% IRR) and 1054% (63% IRR) in 3 and 5 years respectively!

And there you have it!

I hope you have found this interesting. As a reminder, please do your own due diligence regarding this company and formulate your own opinions of what has been said here.